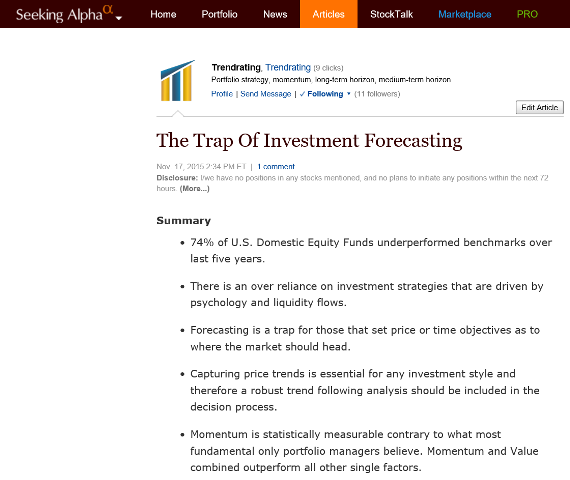

Summary

- 74% of U.S. Domestic Equity Funds underperformed benchmarks over last five years.

- There is an over reliance on investment strategies that are driven by psychology and liquidity flows.

- Forecasting is a trap for those that set price or time objectives as to where the market should head.

- Capturing price trends is essential for any investment style and therefore a robust trend following analysis should be included in the decision process.

- Momentum is statistically measurable contrary to what most fundamental only portfolio managers believe. Momentum and Value combined outperform all other single factors.

The Fund management industry needs to reinvent itself as mutual fund companies continue to lose investors to ETFs because performance hasn’t changed in over a decade. According to S&P, 73.56% of mutual funds in the “all U.S. domestic equity funds” category underperformed over the last 5 years and 85.92% across 3 years for the period ending mid-2014. How is it that the majority of active global mutual funds systematically underperform their relevant benchmarks? And what can be done to enhance profitability?

One explanation can be the combination of two dominant elements: the tendency to fall into the trap of investment forecasting and a heavy reliance on investment strategies that apparently make sense but are less and less linked to the real behavior of a market more and more driven by psychology and liquidity flows.

Human nature is a primary enemy to performance. One of the consequences of real-time market data feeds is that investment managers can make short-term decisions based on emotions (overconfidence, fear, disposal effect, etc.) verses factoring in a longer-term strategy. To that end, the prominent trap to a professional money manager’s performance is primarily the tendency to forecast. Forecasting is not only a trap for those that set price or time objectives but also those that get fixated on numbers as to where the market should head.

But there is another form of forecasting, when fund managers fall in love with a strategy or a style written in stone, with 100 percent conviction that it will work. But, how long will it take to prove that it works? For example, a value-oriented strategy may produce superior returns over time, but how long will it lag behind the performance of an index fund? Will investors patiently sit and wait, sometimes for years? As evidenced by the recent boom in ETFs, it is apparent that mutual funds have lost their mass appeal.

Rigidly sticking with a single investment approach is another way to fall into the trap of forecasting. In this case, the manager or strategist making the forecast cares more about the fact that markets will agree with the merits of their investment strategy instead of the actual outcome. This was the case with Apple during 2014 when many mutual funds either held or reduced their positions in a stock they felt was overstretched from a fundamental perspective. Regardless of their balance sheet, Apple posted a 37 percent gain and continued to post a high momentum rating.

Why aren’t more professional investors then expanding their approach to incorporate intelligent trend following techniques such as momentum factor investing? It could be resistance to change as has been the case with many innovations that have changed Wall Street for the better. It could be good investment intentions combined with lack of education on the true potential of alternatives. Whatever the reason, these managers will soon be on the outside looking in as a younger generation of professionals driven by data in all aspects of their life will attract the wealth of high net worth Millennials who demand more transparency and justification from their advisor’s investment decisions.

Instead of forecasting, mutual fund companies can avoid these traps through a sound momentum model. Successful investing is capturing price trends at the end of the day and therefore a robust trend assessment should be part of any decision process. As market data becomes increasingly real-time, that does not mean that investment decisions should be made with short-term time horizons. Many managers are missing an opportunity to expand their arsenal of tools and to enhance their market data analysis.

Smart momentum tools just react, usually in time, to an emerging trend to allow fund managers to spot major reversals and therefore readjust their portfolio strategies. Momentum does not care about the “why” (why a new trend started will be elegantly explained by analysts after it happened). Momentum points out the “what”. A good model rides trends knowing that trends have a high statistical expectancy to continue for some time and adjusts for market volatility. Momentum is statistically measurable contrary to what most fundamental only portfolio managers would lead investors to believe. Momentum is not based on a gut feel. It’s proven that the combination of value and momentum investing has outperformed each philosophy on its own merits. The negative correlation of value and momentum when used together is tough to beat.

Moreover, momentum investing does not require fund managers to change their approach. They should absolutely start with the investment unit they like, as momentum is not a substitute for fundamental decisions in the investment universe. It is just a way to capture the best trends and avoid the bad trends. What smart momentum is doing is analyzing the momentum between supply and demand using a number of indicators for a refined model that identifies bull and bear trends. It is then up to the fund manager to react to the market data trend.

As a prime example, Goldman Sachs Asset Management just jumped into the ETF business with their ActiveBeta US Large Cap Equity ETF, which should indicate where the industry is headed. The strategy is primarily based upon investing in companies with good value and strong momentum.

As fund managers face a difficult investment environment, it will be interesting to see if the active mutual fund industry as a whole realizes that it’s time to add momentum analytics to their decision support arsenal to try and shift the statistics of performance vs. benchmarks before ETF Issuers eat their lunch. Those that use these tools in addition to their existing market data analysis, will be able to benefit from another technique to close the benchmark performance gap and drive forward their businesses.